Inevitable. If you have followed the Sprint/Clearwire saga since they were joined with Google, Time Warner, Brighthouse, Comcast, and Intel; it was obvious that Clearwire had a hard road ahead. In yesterday's announcement Erik Prusch indicated the depth of the internal concern; Clearwire had retained an advisor to provide options for restructuring.

Once the carrier consolidation of 2012 occurred, the only path forward I saw for Clearwire was funding minimal operations into the 2014 time frame, with a hope that the other 3 national players would finally need the wholesale access to Clearwire's spectrum. With each of the national players, except Sprint, lining up their LTE capacity growth spectrum, the need for wholesale access to Clearwire's WiMax or planned TDD-LTE network was unnecessary. Clearly Sprint needed Clearwire for its LTE growth spectrum and at $0.21/MHzPOP I believe we will look back 5 years from now and view this was steal. Not only has Sprint put in concrete their LTE capacity growth, but they have cornered the market available spectrum for years to come. When you consider that Clearwire controlled 160MHz of spectrum which could be expanded to nearly 200MHz in most metro areas with additional spectrum leasing and spectrum purchases, Sprint has the only meaninful swatch of "new" spectrum that will come to market in the next 5 years.

I don't see the Broadband Incentive auction, the Dish spectrum, or the recent 3.5GHz spectrum as meaningful for efficient macro network coverage. Those subjects are covered in other blogs.

The purchase of Clearwire does not guarantee smooth sailing for Sprint. Sprint still has very significant short term issues. Their LTE network is 5X5 which is the smallest of any of the national carriers. In addition, their customers with WiMax devices will continue to transition over to this network as they upgrade their devices. Clearwire's TDD-LTE hotspot network is only at the construction start stage, with likely very limited coverage throughout 2013. Clearwire has talked historically about devices arriving for this network 2Q or 3Q 2013. Thus, there won't be any material movement of traffic from Sprint 3G or LTE network until early 2014. From what I experience on my Sprint Samsung S3, the 3G network is already challenged and LTE is not available in my market (Seattle). It will get worse before it gets better.

When Clearwire first offered wholesale access to its spectrum, it was using the WiMax technology. It had built this technology in the 2.5GHz band and it was covering up to 80 markets by the end of 2010. At this time Clearwire provided meaningful WiMax coverage in each of their markets for Sprint, Comcast, Time Warner, and Best Buy to provide their customers 4G Only WiMax devices. Essentially, Clearwire's WiMax network had broad enough coverage that these operators could selectively offer their customers service in the markets that Clearwire offered WiMax service.

As Clearwire has embarked on the TDD-LTE strategy, their wholesale model has gotten a bit more complex. First, they continue to sign up relatively small partners for their WiMax wholesale offering: Simplexity, Freedom Pop, Best Buy, CBeyond, Mitel, NetZero, Locus, and Kajeet. They have Sprint already signed for Wholesale Access to the forthcoming TDD-LTE network and added Leap to the WiMax partner list early in 2012.

Leap demonstrates the change of direction for wholesale agreements for the TDD-LTE network. For their TDD-LTE roaming strategy, a roaming partner would need a "thin" LTE network providing coverage in their markets. They would then roam over to the Clearwire TDD-LTE "hot spots" only for capacity. Sprint's 5x5MHz FDD-LTE deployment would qualify as a "thin" LTE deployment. This implicit requirement for a "thin" coverage network, eliminates non-carriers from the TDD-LTE wholesale process since it would be difficult to sell "spots" of coverage across Los Angeles if you didn't have service already over the area.

In addition, the quantity of sites in the Clearwire LTE plan started at 8,000 of their 16,000 sites, was reduced to 5,000 sites and recently has arrived at 2,000 sites. This has increased the challenge of finding wholesale partners with this very limited coverage.

On the surface, a deal to host Dish's spectrum on Sprint's Network Vision platform would make alot of sense. The chart below highlights that part of Dish's (DI) spectrum is adjacent to the AWS-2 spectrum that recently has been referred to as the PCS H spectrum. Sprint is interested in acquiring this spectrum to increase their LTE channel size from 5x5 FDD-LTE to 10x10 FDD-LTE. Unfortunately, the Dish spectrum is configured where the uplink (from the handset to the cell site) would be adjacent to Sprint's LTE downlink (cell site to handset). This will be problematic for Dish. Cell sites transmit at much higher power than handset signals are received. Expensive filters on the separate Dish antennas may not be enough to allow the Dish antennas to be installed in the same plane (level) as the Sprint antennas.

You can look at this as being similar to the Lightsquared deal, except Lightsquared was planned into the deployment through the zoning and permitting process. With the standards body processes that are in front of Dish, it would still be years before equipment is installed and a network operating on Sprint's towers. A Dish MVNO to operate on Sprint's 3G Voice and LTE network would allow Dish to get a wireless product to market quickly.

There were several interesting details that came out of the Deutsche Telekom Capital Markets Day 2012. The primary announcement concerned T-Mobile USA being blessed with the ability to sell the iPhone. T-Mobile's new CEO, John Legere indicated that it will have a dramatically different experience than the other iPhone on the market. In addition T-Mobile will sell it unsubsidized, although they will offer financing plans. This should continue to drive T-Mobile's Cost Per Gross Add (CPGA) down, although they didn't disclose if this only affects their iPhone retail business or potentially all of their retail. This is a dramatic step which eliminate the primary issue that I have had with the subsidy pricing model. I have a problem with paying the same monthly rate for my smartphone if I am out of contract as the guy that who just got a new device. With T-Mobile's plan the true cost of upgrading will be carried by the customer, with the expectation of lower monthly rates.

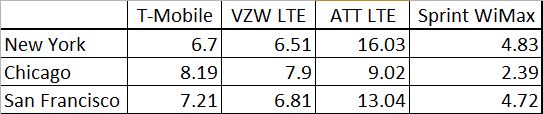

Above is a restatement of the testing data from PC Magazine which T-Mobile released. It is interesting to note how far their speeds have fallen from their early announcements in late 2010 concerning the HSPA+ network. It is also worth noting that they compared AT&T's LTE network. You can again see the loading effect on the network. AT&T's Chicago network was launched September 2011 so it has been loading for over a year reflecting the slower speeds. AT&T's complete New York and San Francisco networks are much newer, launching September 2012, thus carrying less traffic. I am curious why T-Mobile did not chose to compare themselves to AT&T's 4G (HSPA+) network.

From a LTE network build perspective, this was the first time I have heard clearly that T-Mobile is deploying tower top electronics. It is interesting that they state that they are the first carrier in North America to broadly deploy radio-integrated antennas. Clearwire was the first carrier to deploy tower top base stations, followed by Sprint with their Network Vision project. T-Mobile is playing up the fact that their radios are some how integrated into the antenna. Not really an earth shattering announcement. From a technology perspective, deploying the tower top base stations will fill in coverage holes and improve data speeds so it is a good move. In addition, these base stations will be Release 10 capable, meaning a software update will move these radio from the LTE features to the LTE Advance features.

The Numbers:

- Current 4G Network covers 225 million POPs

- Release 10 Equipment being deployed to 37,000 cell sites

- T-Mobile and MetroPCS: Migration not Integration

- With MetroPCS Spectrum Position across Top 25 service areas is improved by 21%

- Planning to shutdown 10,000 macro sites from MetroPCS

- Retain and integrate 1,000 MetroPCS sites

- Operating MetroPCS Markets

- San Francisco

- Detroit

- Boston

- New York

- Dallas

- Atlanta

- Florida (except panhandle)

- MetroPCS brand will increase coverage from 105MPOPs to more than 280MPOPs.