Recent discussions around the wireless industry have included opining on why T-Mobile acquired 40MHz of C-band spectrum when they control so much 2.5GHz spectrum. Although the 2.5GHz spectrum is a valuable spectrum asset, there are two challenges to this spectrum that are not well understood by the industry and we believe that T-Mobile’s C-band purchases were a strategic purchase to provide a path to overcome these two spectrum licensing limitations.

License Areas Controlled by the FCC:

The first limitation is unlicensed or whitespace areas in core urban markets. To highlight these areas, we are going to start with some whitespace analysis that we have developed as part of our EBS Auction Tool. In this analysis, the percentage of the population that is available in the whitespace area is indicated for each EBS channel in a county. We have also calculated the percentage of the population that is contained with T-Mobile license area and the percentage of the population that is contained within the license area of any other carrier. In the image below we are showing the percentage of the population under T-Mobile’s control and under the FCC control (whitespace) for the entire 2.5GHz frequency band including both the EBS and BRS channels. The color ranges start at 0% with red, 50% with yellow, and 100% with green. In our initial analysis we will be focusing on the first auction channel (black box) in the six counties that make up the Chicago CMA market. We prefer to use the CMA market structure to evaluate urban areas because they include only the most populated counties in each urban area.

2.5GHz Full-band Population Percentage View (Chicago):

2.5GHz – 1st EBS Auction Channel Population Percentage View (Chicago):

Chicago CMA Counties:

In the top section of the chart above, it is apparent that T-Mobile controls all of the 1st EBS Auction channel in Cook, DuPage, and Will counties but they only control all of the A1-A2-A3 channels in Kane County. Fortunately, the parts of 1st EBS Auction channel that they don’t own will be available in the Auction 108. The available whitespace is indicated in the lower half of the chart. Looking at McHenry County, 100% of the C1-C2 channels will be available in the EBS Auction (108).

These charts highlights the percentage of the population available either for T-Mobile’s licenses or for the FCC’s whitespace. Next we will look at the geographic constraints of T-Mobile’s licenses and the shape of each county’s whitespace area. In the map below we are able to show the license areas for the A1-A2-A3 channels because the license areas of interest are identical. It is apparent that T-Mobile has the rights to operate the A1-A2-A3 channels completely across the counties in the Chicago CMA except Lake and McHenry.

Licensing Map – A1-A2-A3 (Chicago):

Looking at the B1-B2-B3 & C3 channels, a whitespace area exists covering almost all of Kane County along with similar whitespace areas in McHenry and Lake counties.

Licensing Map – B1-B2-B3 & C3 (Chicago):

Our final map delineates the largest limitations to the areas that T-Mobile can deploy the C1-C2 channels in the Chicago CMA market. Their base stations located in the gray areas of Kane, Lake, and McHenry counties cannot use the C1-C2 channels.

Licensing Map – C1-C2 (Chicago):

Looking again at the T-Mobile’s control of the 1st EBS auction channel we can highlight the deployment limitations that the whitespace area presents. Since the 1st Auction channel is 49.5MHz, this chart indicates that T-Mobile can deploy roughly a 50MHz channel on any sites in Cook, DuPage, and Will counties. In Kane County they are limited to a 15MHz channel in the available 16.5MHz of spectrum. To have a consistent deployment of a 50MHz channel across Chicago, they would need to purchase the whitespaces areas for each of these channels in each of the Chicago counties.

Looking again at the T-Mobile’s control of the 1st EBS auction channel we can highlight the deployment limitations that the whitespace area presents. Since the 1st Auction channel is 49.5MHz, this chart indicates that T-Mobile can deploy roughly a 50MHz channel on any sites in Cook, DuPage, and Will counties. In Kane County they are limited to a 15MHz channel in the available 16.5MHz of spectrum. To have a consistent deployment of a 50MHz channel across Chicago, they would need to purchase the whitespaces areas for each of these channels in each of the Chicago counties.

The last perspective that we want to share on the Chicago market is the actual population in each of the whitespace areas for each county. Although we thought that 100% of the population was available for each channel in Cook County, the whitespace population table indicates that there is a very small population and small geographic area that is a whitespace within Cook County for the B1-B2-B3-C1-C2-C3 channels.

2.5GHz – 1st EBS Auction Channel Population View - Whitespace (Chicago):

License Areas Controlled by Other Carriers:

The second limitation is spectrum blocks that are controlled by other carriers in core urban markets. To highlight these areas we are going to look at the four counties in the Los Angeles CMA market. For the Population Percentage Chart below, we are including the population percentage for other carriers rather than the whitespace percentages.

2.5GHz Full-band Population Percentage View (Los Angeles):

2.5GHz – 3rd EBS Auction Channel Population Percentage View (Los Angeles):

In the Top View it is apparent that T-Mobile already controls the spectrum across all of the BRS channels (gray) in Los Angeles County but they are missing roughly 10% of the population for the G1-G2-G3 channels. In between the two BRS blocks of spectrum are the K guard band channels. The ownership of these guard band channels mirrors the ownership of the primary channel e.g. G1=KG1. The BRS channels and the EBS G1-G2-G3 channels total to 87MHz of spectrum, providing T-Mobile the ability to deploy an 80MHz NR channel throughout most of Los Angeles County. Unfortunately in Orange County, another carrier owns 98% of the G1-G2-G3 channels limiting T-Mobile to a 10MHz channel in the first BRS block (F4-E4) and a 50MHz channel in the second BRS block (BRS2-E123-F123-H123).

Los Angeles CMA Counties:

In looking at the G1-G2-G3 licensing map, you can see that there are actually three licenses that T-Mobile does not control in the Los Angeles CMA Market.

Licensing Map – G1-G2-G3:

2.5GHz – 3rd Auction Channel Population View – Other Carriers (Los Angeles):

The Other Carriers Population percentage view indicates the large licensed population that is controlled by other carriers and would need to be purchased by T-Mobile.

Conclusion:

With these two examples we have shown that missing 2.5GHz spectrum either due to it being unlicensed or being controlled by another carrier present challenges that likely limit T-Mobile’s largest 5G channel size to a subset of each urban market. We believe that T-Mobile’s participation in the C-band and the current 3.45GHz auction was to “future” proof their ability to offer large channel sizes in the upper mid-band spectrum. With either the C-band spectrum or the 3.45GHz spectrum, T-Mobile could use carrier aggregation to achieve 100MHz effective channel sizes even in areas where their 2.5GHz spectrum is more limited.

There is a little buzz this morning about an application from Google to construct a experimental network on 2.5GHz frequencies on the Mountain View, CA campus. Here is a

link to the application. The application states that they will be using spectrum between 2.524 and 2.546GHz and between 2.567 and 2.625GHz. The top issues with this application is that Clearwire operates their WiMax network within this market and has states on their earnings calls that they typically deploy using between 30MHz and 60MHz of spectrum. Google would need to guarantee that there would be no harmful effect to this commercial network. Now lets look at the specific spectrum allocations.

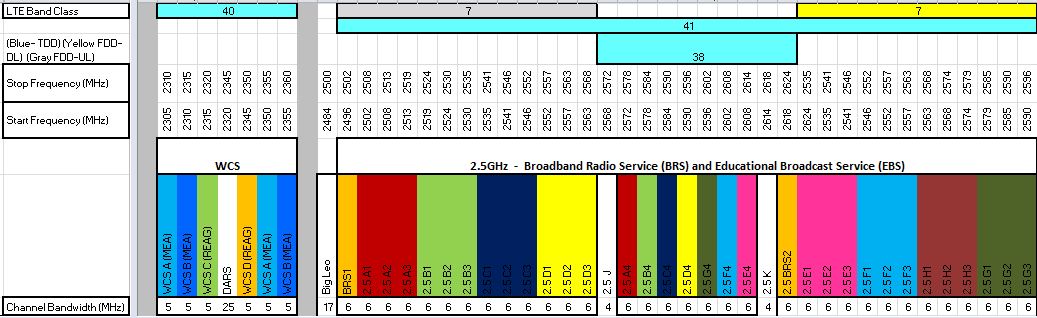

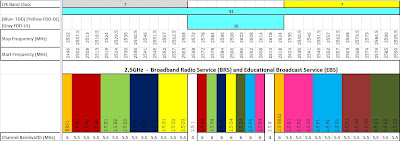

In the above image from my Spectrum Ownership Landscape Report, you can see that the lower band matches correctly to the B2, B3, C1, and C2 channels. The upper band matches the LTE Band 38 so there would appear to be a desire to test TDD-LTE equipment in that portion of the band.

Can Google do this without Clearwire's agreement and assistance? I don't think so. The B2,B3 channels are owned by The Santa Clara Board of Education (Call Sign WHG338) and don't appear to be leased to Clearwire so they are ok. C1,C2 (Call Sign WHR466) are owned by The Assocation for Continuing Education and they appear to be leased to Clearwire. The spectrum in Band 38 is particularly interesting. First of all, it is the portion of the spectrum that is currently dedicated to video operation, so Google would need to work with each of the broadcasters and convince them that their operation in Mountain View would not interfer with the ability of the broadcaster's clients to receive their desire video broadcast. In addition, the presence of this high powered video interference would make Google's tests much more challenging, especially outdoors. On the far right of the spectrum allocation Google has requested is the BRS2 channel that is clearly owned by Clearwire.

For the video spectrum, Clearwire still holds the leases for the A4, C4, D4, E4, and F4 channels. I anticipate that Clearwire is not supportive of this testing without their involvement and they will protest the experimental authorization. In my history with with wireless carriers, it was not unusual to see a experimental application for my carrier's spectrum without being contacted directly for the use of my carrier's spectrum.

Globalstar's Proposed Terrestrial Low-Power Service (TLPS) has some well thought-out approaches. Globalstar has petitioned the FCC to allow them to utilize their 2484-2500 MHz "Big Leo" satellite spectrum to provide terrestrial coverage.

Globalstar's spectrum lies directly above the 2.4GHz ISM band which hosts a vast majority of the WiFi in use today, as well as bluetooth and microwave ovens. Directly above the Globalstar spectrum is the EBS/BRS spectrum controlled primarily by Clearwire.

Globalstar has proposed terrestrial operation on a the newly named AWS5 band. It would essentially be a 4th non-overlapping WiFi channel (Channels 1,6,and 11 are the primary non-overlapping WiFi channels). It would still be a 22MHz wide channel, using the ISM band above Channel 11 (which is lightly used) and about 10MHz of their AWS5 channel. Globalstar believes that most existing WiFi devices could support this spectrum with a over-the-air software updates so a massive number of devices could be overloaded to this network once it is constructed.

Also intriguing is the improved performance characteristics of this spectrum. First, since it is licensed to Globalstar, they can control the use of the spectrum. They envision a carrier grade network using this spectrum that would manage Hotspot power levels and interference. Since this spectrum has much less interference, it is capable of covering larger areas with higher speeds than typical WiFi.

If Globalstar can figure out the backhaul aspect to providing this service, I think they will have a leg up on other white-glove WiFi service providers since they are better able to manage the RF environment for their frequencies. It is conceivable that Globalstar would host WiFi overloading for all of the 4 national carriers. I still see the biggest challenge to be in a residential environment where they envision a hotspot in my house being under their control, but likely on my cable internet service. I'm pretty sure Comcast won't react well to my residential internet service supporting a commercial operation.

Is this a service that could be considered or expanded into the EBS/BRS channels that are adjacent to Globalstar's spectrum? The answer is yes. Clearwire has stated that they have excess spectrum. I would anticipate that this would look like a private LTE network on Clearwire's spectrum versus WiFi on Globalstar's, but it would not be as feasible as Globalstar's proposal due to the current lack of devices that support LTE on the EBS/BRS frequencies.

Dish's counter-offer for Clearwire is intriguing. I recently completed a presentation detailing the challenges of a spectrum sale in the EBS/BRS spectrum. Clearwire's press release states that this offer was on the table when Sprint's offer was received but Sprint's offer was deemed better.

Tim Farrar's Blog indicates that the spectrum sale would likely be for Clearwire's BRS spectrum. This is a realistic assumption. In my presentation (linked in a previous blog) I highlighted that one of the primary problems with the leased spectrum is that it has limited geographic coverage, covering many of the dense metro areas but not contiguous all the way to a county or BTA border. There are still a few elements of a BRS spectrum sale that should be understood.

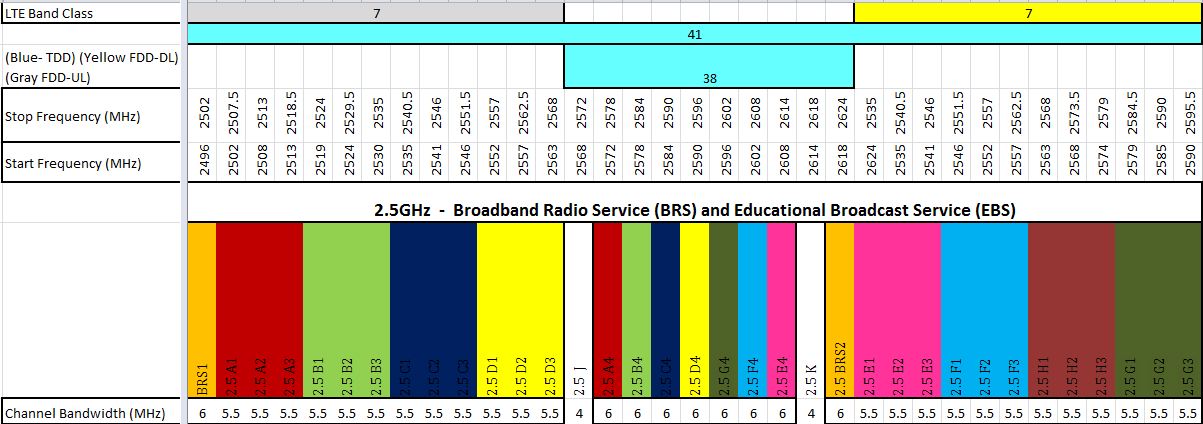

From the image above, the BRS spectrum sale would include the Orange (BRS1/BRS2) channels, the Pink (E channels), Light Blue (F channels) and Brown (H channels). This would equate to one contiguous block of 55.5MHz of spectrum, a 12MHz block of spectrum (E4,F4), and the isolated BRS1 channel. The 12MHz block could only be used if mid-band video operations have ceased in a market. Currently, I don't believe that any of the Top 10 markets have completed ceased video operations. The 55MHz of spectrum can support 2 - 20MHz TDD-LTE channels. This would virtually eliminate the ability to utilize the EBS/BRS spectrum for any FDD-LTE operations. It may be possible with a guardband in the H channels to operate the D channels and G channels in a FDD-LTE configuration.

In looking at the LTE Bandplans, the potential Dish spectrum allocation would miss the international TDD-LTE Band 38 which Softbank, China Mobile, and the UK auctions are using. We will have to watch carefully to see if international devices will include functionality of Band 41.

My last area of concern is whether that will leave enough spectrum for Clearwire to continue to operate their WiMax network as they bring their TDD-LTE network online. Additionally, with the geographic limitations of the leased channels, there may be a limited number of sites operating on Clearwire's network today, that won't have available spectrum without the owned channel spectrum.

Below is a link to an Investor's Presentation provided by AllNet Labs detailing the licensing, geographic, and leased versus owned challenges of Clearwire's Spectrum.Audio and Slide PresentationPresentation Outline

Agenda- History of the EBS/BRS Spectrum

- Owned versus Leased Spectrum

- LTE Band Configuration

- Recent Auctions

- Substantial Service

- Issues before the FCC

- Spectrum Sale Challenges

Another area of interest from the Sprint / Clearwire conference call yesterday were Erik Prusch's comments related to Clearwire's attempts to sell spectrum in 2010. Erik indicated that the offers they received were below value.

I will be conducting a webinar for GLG Research on January 4, 2013 where I will be discussing the history and challenges of Educational Broadcast Service (EBS) and Broadband Radio Service (BRS) spectrum. I believe that the undervalue offers were due to issues with the spectrum channelization, geographic boundaries, unlicensed channels, and FCC mandated obligations for leased spectrum.

Clearly the wireless industry has locked in spectrum pricing with the MHz-POP pricing model, but is this the right way to look at it as we move into a 4G World where data throughput and capacity are key? For those that aren't familiar, the typical value of spectrum is determined by the $/MHzPOP which is the dollars spent for the spectrum divided by the total amount of spectrum times population that spectrum covers. This model falls short now as carriers are interested in acquiring larger contiguous blocks of spectrum enabling higher users speeds and more capacity.

To use a real estate analogue, a large plot of land is much for flexible for multiple uses, than two plots, even if they are in the same neighborhood. In real estate, the developer that is able to consolidate several tracks of land into a larger development is rewarded as he sells the larger development.

In the wireless industry, we continue to price based upon the $/MHz POP basis, even as carriers such as T-Mobile and Clearwire have combined adjacent channels to create larger bands of spectrum to utilize in larger LTE channels. T-Mobile has worked this year with Verizon, SpectrumCo, and MetroPCS which will allow it to assimilate a 2X20MHz LTE channel on a national basis. Clearwire has leased and purchased operators in the BRS and EBS spectrum bands providing it with an average of 160MHz of spectrum in the top markets. Since Clearwire's spectrum has many geographical boundaries, it is difficult to say how many 20MHz channels they could support across each of their markets, but they have been successful consolidating small bands of spectrum into larger more flexible spectrum bands.

How does a larger band of spectrum affect the wireless carriers? In the US, carriers have deployed FDD-LTE in 1.25MHz channels, 5MHz channels, and 10MHz channels. As you increase the channel size throughput performance improves because a lower percentage of the data packets are dedicated to overhead activities Qualcomm has provided achievable LTE Peak Data Rates for different channel bandwidths based upon whether the antennas are 2x2 or 4x4 MIMO.

Link to Qualcomm DocumentAs you can see in the 4x4 MIMO downlink case, the throughput is 12Mbps greater in the 20MHz channel than the composite of 4-5MHz channels.

So if a 20MHz channel is 4% more efficient than 4 - 5MHz channels should the MHz POPs pricing adjust accordingly?

By the way.. I am going to look for more source data on the capacity improvements for wider channels, a 4% improvement would seem to be relatively negligible. I recall hearing 30% improvements in capacity when a channel size is doubled, but I haven't been able to re-source that data for this blog. More to come.